I have previously written about the fiscal crisis facing Medicare and Medicaid. In Part 1, I wrote about the extent of the trouble that the United States finds itself in when it comes to financing Medicare and the “dual eligibles” who also receive Medicaid benefits for the future. In Part 2, I wrote about the origins of the problems that these programs face as well as the inaccurate forecasts of just how much these programs would cost.

Now I’ll finish up this series by talking about where we need to go from here.

But, first, a little news to set the stage.

A marriage made in red tape

Right now, two of the nation’s largest private health insurance companies – Anthem and Cigna – are trying to merge and become the very largest private health insurance company in the nation. The merger is pending, which is akin to an engagement prior to a wedding.

As a former Anthem employee, I’m totally rooting against for this despicable lovely couple. They most certainly deserve each other. But if these two companies are getting married soon, they may want to see a counselor to talk about their issues.

Akin to learning that your fiancée has a criminal history just before the wedding, Cigna just got busted by the Centers for Medicare and Medicaid Services (CMS) for its handling of Medicare Advantage (MA) and Medicare Part D prescription drug plans for doing all the things that private insurance companies are infamous for doing: denying health care services and prescription drugs to patients who needed and should have received them and mishandling the grievance and appeal process.

Cigna has had a longstanding history of non-compliance with CMS requirements. Cigna has received numerous notices of non-compliance, warning letters, and corrective action plans from CMS over the past several years. A number of these notices were for the same violations discovered during the audit, demonstrating that Cigna has not corrected issues of non-compliance.

Centers for Medicare and Medicaid Services

As a result of this bad behavior, Cigna informed the Securities and Exchange Commission (which would be akin to the wedding officiant, I suppose) that it couldn’t sell new MA or Medicare Part D policies.

But wouldn’t it be hypocritical for Anthem to break off the wedding? After all, Anthem (which was known as WellPoint at the time) got into the exact same predicament with CMS in 2009 due to similar bad behavior. Eventually those sanctions were lifted, but there was some lost revenue in the meantime.

Considering how lucrative managing these plans has been for private insurance companies, the new restrictions on Cigna could, at the very least, put a damper on the couple’s honeymoon plans.

Private insurers worsen fiscal crisis

For all of the problems that MA and Medicare Part D enrollees have experienced due to bad behavior on the part of the private insurers who operate the plans, you would think that Medicare Advantage would be saving taxpayer dollars in the Medicare Trust Fund.

You would be wrong.

Our findings indicate that the inclusion of private plans in the Medicare program has cost taxpayers $282.6 billion, or 24.4 percent of the total amount Medicare has paid private plans since 1985. Our findings likely underestimate the magnitude of the overpayments…

…In 2012 alone, we estimate that private insurers are being overpaid $34.1 billion, or $2,526 per MA enrollee…

..Advocates of market-based Medicare reforms suggest that competition among private plans will induce greater efficiency and result in cost savings. Our findings indicate that the opposite is true. Private plans have drained more than $280 billion from Medicare since 1985, most of it in the last eight years. Increasing private enrollment through voucher-type Medicare reform (as suggested by Republicans) or through quality bonuses and financial incentives to plans to enroll dual-eligible beneficiaries (as enacted by President Barack Obama’s administration) will almost certainly raise Medicare’s costs, not lower them.

Funds wasted on overpayments to private MA plans could instead have been used to improve benefits for seniors, extend the life of the Medicare Trust Fund by more than a decade, or reduce the federal deficit. Private insurers have enriched themselves at the expense of the taxpayers.

Hellander, et al. Medicare overpayments to private plans, 1985-2012: Shifting seniors to private plans has already cost Medicare US$282.6 billion. International Journal of Health Services 2013; 43(2): 305-319.

Just to be clear, that means overpayments have amounted to about one fourth of all the payments made from taxpayers to private health plans to cover Medicare beneficiaries. And this is estimating conservatively.

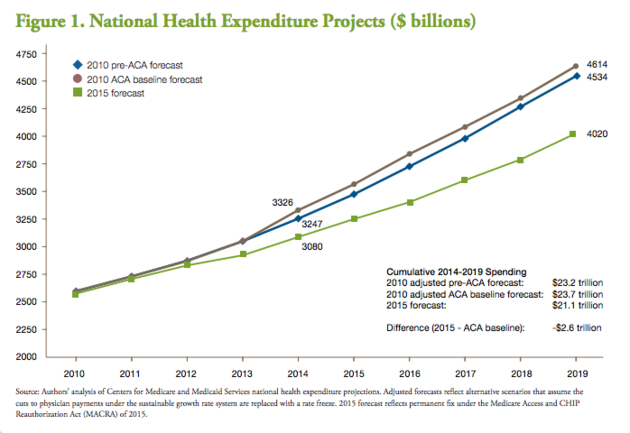

The entire health system is sick, and the Doc Fix was no cure

As I’ve written before, the entire U.S. health system is burdened by an inordinate amount of wasteful spending that doesn’t improve anyone’s health. It’s impacting all health payers, not just Medicare and Medicaid.

Whereas private insurers have responded to increased health spending by increasing premiums — which they must do in order to turn a profit, stay afloat or even maintain the cash reserves required by insurance law — the Medicare Trust Fund doesn’t even remotely work that way.

Changing any Medicare or Medicaid formula, from taxes to provider reimbursement to benefits, requires an act of Congress and a debate that most politicians of all stripes would prefer to avoid.

When it comes to Congress’s action on provider reimbursement in Medicare, it’s a good news/bad news/good news scenario.

The good news: In 1997, Congress and President Bill Clinton enacted a Sustainable Growth Rate formula that indexed physician reimbursement in Medicare based on the rise (or fall) of the nation’s gross domestic product. If physician spending grew more slowly than the GDP did, physicians got a raise. If physician spending grew faster than the GDP did, physicians had to take a pay cut.

The bad news: This seemed reasonable in 1997 when GDP was growing rapidly and provided some cost control incentives to counterbalance the perverse incentives of the fee-for-service model. But, after the 9/11 attacks, the economy stagnated, and physicians felt a considerable pinch. After all, the broader economy was largely outside of each physician’s control, as were the actions of other physicians. The financial crisis of 2008 and the resulting recession would have really made things uncomfortable for physicians under the SGR…including a potential 21 percent pay cut in 2010.

So, from 2003 to 2015, the American Medical Association successfully lobbied Congress each year to bypass the SGR and give physicians a raise regardless of what happened with GDP. This was known as the “Doc Fix,” and it had to be renewed each year. As you might imagine, when you ignore the Sustainable Growth Rate formula for years, you end up with a growth rate that is not sustainable. And that’s indeed what happened – at a cost to taxpayers of $150 billion.

The good news: Just about everyone realized that this cut-and-paste formula of passing a new Doc Fix bill every year just to bypass the SGR was inefficient, expensive, and absurd.

So, in 2015, Congress and President Obama struck a deal to permanently eliminate the SGR and create a new reimbursement formula tied to quality of care and efficient use of resources. This was considered to be a permanent Doc Fix.

Without digging too far down into the weeds, suffice it to say that it sounds like we’re finally getting somewhere for reforming Medicare and reducing waste in the health care system. But I’ll believe it when I see it.